Data tokens on this page

Weekly Wealth Wire

Weekly Wealth Wire

U.S. Treasury note yields finished the week down with the 10-year Treasury note yield declining the most in one month since August of last year. On the other hand, equities surged last week on comments by Federal Reserve chairman Jerome Powell that the current benchmark rate was “just below” neutral, implying the central bank could be close to leaving interest rates steady. As recently as last month, Mr. Powell had said rates were “a long way” from neutral. Along with tariffs, fears of higher interest rates, which could lead to slower growth, remains a key concern for most investors.

In economic news, real GDP grew at a 3.5% annual growth rate in the third quarter, matching the initial estimate as well as consensus expectations. Pre-tax corporate profits grew by 3.4% in the third quarter, the fastest quarterly growth rate since the second quarter of 2014, and are up 10.3% in the past year, the largest four-quarter increase since mid-2012. New single-family home sales declined 8.9% in October to an annual rate of 544,000, missing consensus estimates. Personal income increased 0.5% and personal consumption increased 0.6% in October, both beating consensus estimates. Housing numbers remained disappointing as new home sales came in under expectations for October and continued to soften. Rising costs due to material and labor shortages coupled with higher interest rates have driven down home affordability.

Looking ahead, all focus will be on fallout from this past weekend’s dinner at the Group of 20 where Presidents Donald Trump and Xi Jinping were in attendance. If no resolution is reached soon, 25% levies are set to be placed on Chinese goods starting January 1st.

The Week Ahead

Key Economic Reports

- October Factory Orders

expected: -2.0%; prior: 0.7%

- November ISM Index

expected: 57.2; prior: 57.7

- November ISM Services expected: 59.0; prior: 60.3

- November Unemployment

expected: 3.7%; prior: 3.7%

- November Nonfarm Payrolls

expected: 189k; prior: 250k

- November Private Payrolls

expected: 185k; prior: 246k

- November ADP Employment Change

expected: 192k; prior: 227k

- December Michigan Sentiment - prelim

expected: 96.8; prior: 97.5

VITAL SIGNS

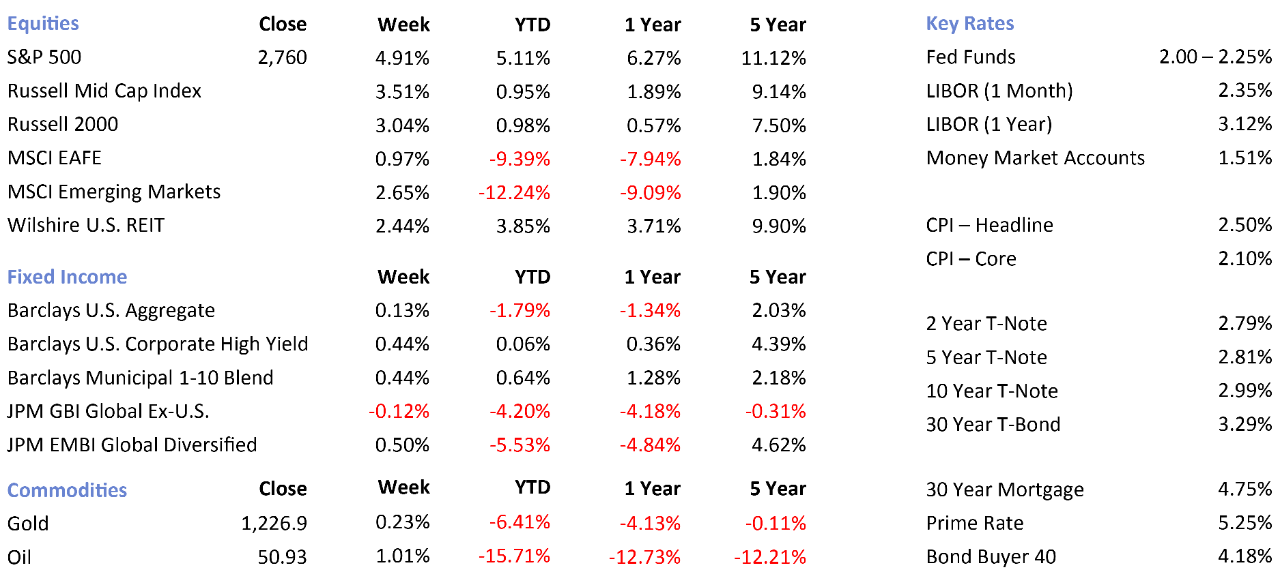

Sources: briefing.com, Yahoo Finance, Kitco.com, U.S. EIA, First Trust, Wintrust Wealth Management analysis. Returns are total returns calculated through 11/30/2018 and 5 year returns are annualized. Gold is the New York spot price in $/oz. Oil is the Cushing, OK WTI spot price FOB in $/BBL. Securities, insurance products, financial planning, and investment management services are offered through Wintrust Investments, LLC (Member FINRA/SIPC), founded in 1931. Trust and asset management services offered by The Chicago Trust Company, N.A. and Great Lakes Advisors, LLC, respectively. ©2018 Wintrust Wealth Management

Investment products such as stocks, bonds, and mutual funds are:

NOT FDIC INSURED | NOT BANK GUARANTEED | MAY LOSE VALUE | NOT A DEPOSIT | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY